Au Revoir: Why the Old Inflation Environment May Be Gone for Good

The U.S. 30-year Treasury yield and the U.S. 10-year Treasury yield recently crossed the 5% and 4.5% marks respectively. Like any other number, the thresholds are arbitrary, but notably, yields on these securities have not reached such levels since the onset of the global financial crisis in 2007.

Recently, I had the privilege of watching the Western Conference Finals between the Oklahoma City Thunder and San Antonio Spurs. As a Boston native and lifelong Celtics fan, it is with great remorse that I’ve come to acknowledge it may be far more difficult for the Celtics to bring home another title anytime soon. Unfortunately for Boston, there is now a 7’5” giant looming in the Western Conference, and this series proved that Victor Wembanyama is no longer just a future problem for the rest of the league. He is already a current one, and the NBA has entered a new era.

Unlike the joy I had celebrating the Celtics title in 2024-2025, I could not realize many of the benefits that came from the post-2008 interest rate environment, or even the post-Covid rate environment for that matter. Those of you who own homes had the opportunity to refinance at rates as low as 2.5%-2.75%. Truly a “once-in-a-lifetime" opportunity. But the point isn’t that rates are higher today; it’s to look at why they are higher. Higher rates are only the most visible part of the shift and the inflation environment that helped push them there may be harder to fully leave behind than many investors had thought.

Higher Prices

I’d like to start with a “vibe-check” on consumers. One-year inflation expectations have climbed to their highest level since 2022, which coincidentally was also the last time we experienced a major war-related energy shock. What can make inflation difficult to explain is that the data measures the rate of change, not whether prices are returning to where they were before. Even when inflation slows, prices do not automatically, or typically, reset to where they were before. They continue building off a higher base. That is why inflation can feel like a constant pressure on consumers, even after the worst of the initial shock has passed. Again, as shown above, consumers are seemingly left questioning whether meaningful relief is coming anytime soon.

Source: Federal Reserve Bank of Cleveland via FRED

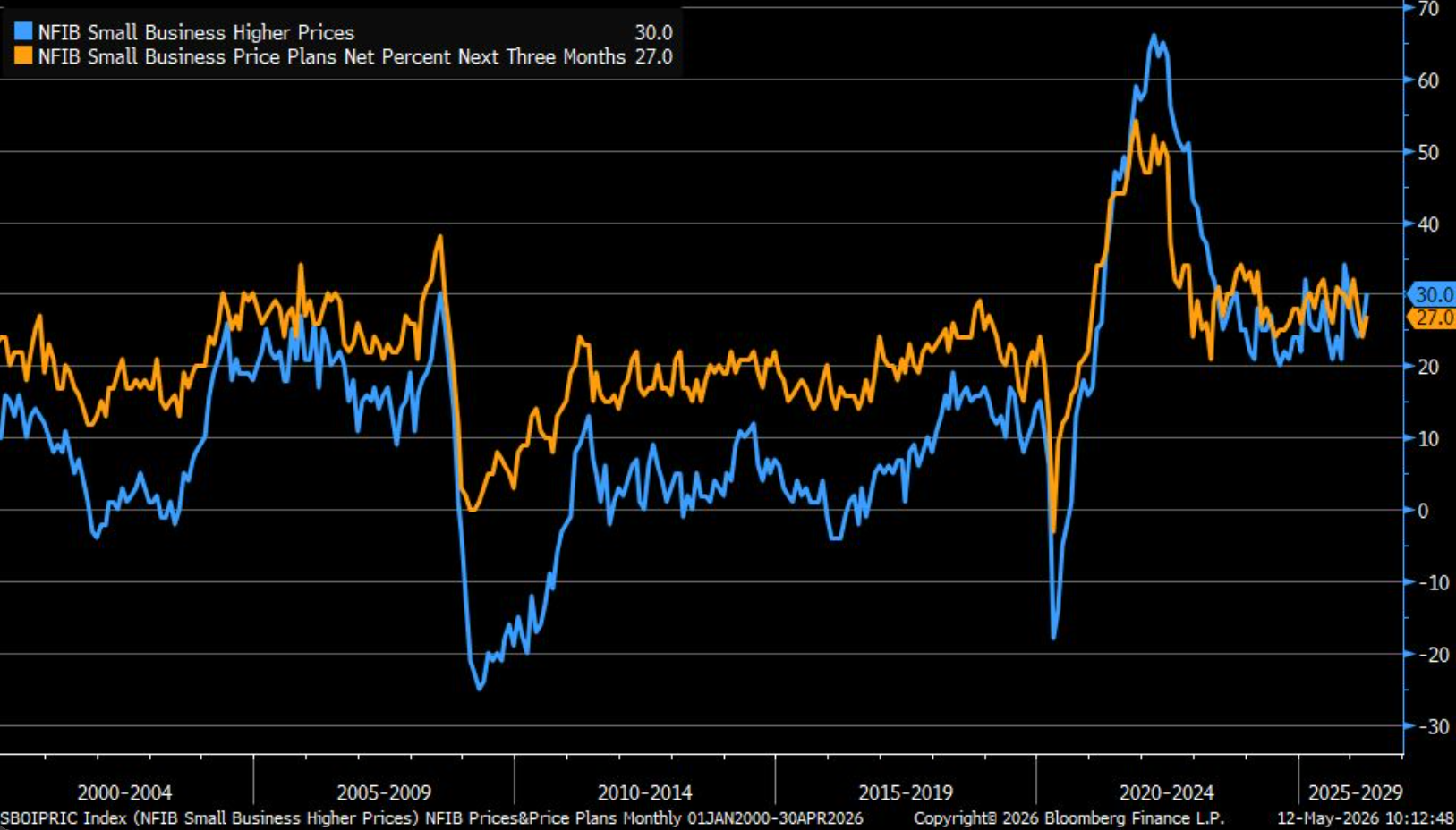

Pressure on Businesses

The next place to look at is the business side of the economy. Consumer expectations matter because they help show how households are feeling, but inflation ultimately becomes more persistent when businesses are forced to accommodate higher costs into their pricing decisions. That is especially true for small businesses with tighter margins which tend to feel changes in wages, rent, insurance, energy, and supplier costs more directly. With that, the small business side of things seems to be echoing a very similar sentiment. According to the National Federation of Independent Business (NFIB), roughly 30% of small business owners reported raising prices in April while another 27% of small business owners have plans to raise prices in the next three months.

A lot of these price changes can take a while to trickle through the economy. That is the part that makes inflation difficult to dismiss. The first wave is easy to see. The second wave is slower and less obvious. It can show up through higher shipping costs, wages, insurance, and businesses gradually adjusting prices to protect margins. By the time those costs reach the end consumer, the initial headline may feel old, but the impact continues to work its way through.

Source: Liz Ann Sonders LinkedIn per National Federation of Independent Business (NFIB)

Preserving Purchasing Power

This doesn’t stop with consumers; it also matters to us as investors and how we think about cash, portfolios, and long-term purchasing power. At its very simplest, inflation eats away at the purchasing power of cash over time. Although cash can often feel “safe,” it is important to make sure every dollar has a purpose. That purpose may be liquidity, income, growth, or long-term purchasing power. A surprisingly common mistake is keeping too much money in low-interest savings accounts, even when that cash could be earning a much more competitive rate in a money market fund or another appropriate short-term vehicle. Many investors fall prey to this, and the cost can add up to thousands of dollars over a lifetime. For money that needs to remain available, at a minimum we can make sure cash is not sitting idle while inflation continues to erode its value. For money intended to fund longer-term goals, it means maintaining exposure to assets that have a reasonable chance of outpacing inflation over time, such as equities.

A different era changes expectations. Inflation may be well below its 2022 peak, but the path back to a more comfortable environment still looks uneven. Our job as advisors is to help clients plan realistic assumptions and make sure their cash, portfolios, and broader financial plans are aligned with the environment we are living through. If higher prices remain a recurring pressure, discipline is essential as well as making sure every available dollar has a purpose.