Your financial life is complicated, and it pays to automate and simplify it.

While automation can streamline our finances, it’s essential to monitor your accounts regularly to detect any irregularities and ensure everything is running smoothly.

Your financial life is complicated, and it pays to automate and simplify it.

While automation can streamline our finances, it’s essential to monitor your accounts regularly to detect any irregularities and ensure everything is running smoothly.

The US equity market posted negative returns for the quarter and outperformed non-US developed markets, but underperformed emerging markets

Interest rates increased across all bond maturities in the US Treasury market for the quarter

Emerging markets posted negative returns for the quarter and outperformed both US and non-US developed markets.

In the past century, there have been 15 recessions in the US. In 11 of those instances, stock returns were positive two years after the recession began.

Stock markets typically drop well before a recession is officially announced and then rebound before the recession is officially over.

Commit to holding onto your portfolio’s stock allocation for the long term and rebalancing it if markets drop due to a recession or any other event that may trigger a bear market

The US equity market posted positive returns for the quarter and outperformed both non-US developed and emerging markets.

US real estate investment trusts outperformed non-US REITs during the quarter.

The Bloomberg Commodity Total Return Index returned -2.56% for the second quarter of 2023.

Every family should create a Family Emergency User Manual. This is your family’s financial and operational blueprint in case an unexpected crisis happens.

Communicate or leave a Trail on How to Find your User Manual.

Consider gifting to family members or charities during your life so you’re able to enjoy seeing others benefit from your generosity.

The US equity market posted positive returns for the quarter and underperformed non-US developed markets, but outperformed emerging markets.

REIT indices underperformed equity market indices.

Across equities, Value and Small caps underperformed Growth and large caps.

The US equity market posted positive returns for the quarter and underperformed both non-US developed and emerging markets

Emerging markets posted positive returns for the quarter and outperformed the US market, but underperformed non-US developed markets.

The Bloomberg Commodity Total Return Index returned +2.22% for the fourth quarter of 2022.

2022 was the seventh worst calendar year loss for the S&P 500 Index since the 1920s, down -18.1%.

The 13% drop in the Aggregate Bond Index for the year was over 10% greater than any other annual drop in this index’s history!

Since 1928, the S&P 500 Index has experienced two or more consecutive negative years just eight times.

Develop the habit of reviewing your estate planning documents and beneficiary designations on a regular basis. We recommend doing this at least every two to five years at a minimum and always after any significant life event.

Even a young adult should have the following estate planning documents: Advanced Health Care Directive, Financial Power of Attorney, Beneficiaries for accounts, Last Will and a Digital Will.

The US equity market posted negative returns for the quarter and outperformed both non-US developed and emerging markets.

The Bloomberg Commodity Total Return Index returned -4.11% for the third quarter of 2022.

US real estate investment trusts outperformed non-US REITs during the quarter.

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.” – Peter Lynch

Make sure you have enough cash and other conservative investments so you will never have to sell stocks in a bear market even a prolonged bear market.

Expect stock markets to fall further after you rebalance, in other words mentally prepare for this so you will not be overly bothered by it.

US mortgage rates hit 5% for first time since 2011.

The US equity market posted negative returns for the quarter and underperformed both non-US developed and emerging markets.

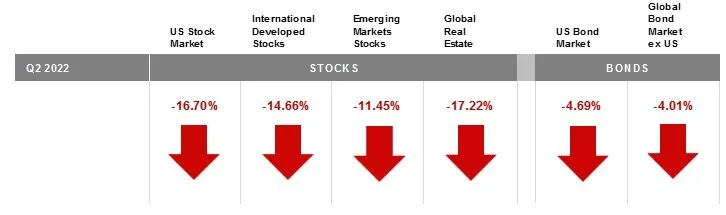

The Bloomberg Commodity Index Total Return returned -5.66% for the second quarter of 2022.

While volatile periods like the one we’re experiencing now can be intense, investors who learn to embrace uncertainty may often triumph in the long run.

One early retirement study noted that a withdrawal rate of 4% is relatively safe.

Many researchers have evaluated withdrawal rates and related issues since then - proposing adjustments to the traditional 4% rule.

One such proposal, the Target Percentage Adjustment (TPA) suggests modifying your withdrawals year by year.

Being flexible in the face of market downturns and inflation can allow you to increase your withdrawals in retirement.

Emerging markets posted negative returns for the quarter, underperforming the US and non-US developed equity markets.

The US equity market posted negative returns for the quarter and underperformed non-US developed markets, but outperformed emerging markets.

The Bloomberg Commodity Index Total Return returned +25.55% for the first quarter of 2022.

Vanguard’s 10-year forecast for U.S. equity returns is 2.3% to 4.3% per year; and for global equities it’s higher at 5.2% to 7.2% per year.

Market corrections are a good time to rebalance your portfolio and add back to stock holdings.

History shows that reaching a new market high doesn’t mean the market will then retreat.

It is wise to have a plan in place for the possibility of reduced future investment returns.

Emerging markets fell 2.5% for the year, underperforming both US and non-US developed equity markets.

The Bloomberg Commodity Index Total Return returned -1.56% for the fourth quarter of 2021.

Interest rate movements in the US Treasury fixed income market were mixed during the fourth quarter.

Single taxpayers with taxable income less than $400,000 and married filing jointly (MFJ) taxpayers with taxable income less than $450,000 should not see much change in the taxes they pay as a result of the changes under the new Biden tax plan.

Some taxpayers with income below $400,000 and $450,000 could see tax reductions due to the return of the state and local tax deduction.

If your income is above this $400,000 and $450,000, expect your taxes to go up.

The US equity market was flat for the quarter and outperformed non-US developed markets and emerging markets

In emerging and developed markets, most currencies depreciated vs. the US dollar

The Bloomberg Commodity Index Total Return returned 6.59% for the third quarter of 2021.